What I’ve learned about the good, the bad, and the ugly Annuities

An annuity is the most hated investment vehicle, yet, the annuities are still being sold.

An annuity is the most hated investment vehicle, yet, the annuities are still being sold.

- There are many negative points in this type of investment but the only positive could be the major one at a certain period of your life.

- Be aware of the complexities of annuities.

- Get educated before choosing any annuities for your portfolio.

- This is a lengthy article, so be patient if you want to learn more.

Let me start with an introduction to annuities made by S. McDonald from the Oxford Club. While I like his articles related to retirement, I don’t like the cost of his offered services but this is another topic. This is when he got it straight:

“Down here in the retirement belt, we have these annoying things called hurricanes. They pop up between June and November and cause all kinds of problems.

Most of the damage they cause is due to flooding. Winds are a problem too, but the flooding will definitely ruin your whole day.

That's why insurance companies have what are called "flood zones" - areas they predict will flood when a storm comes ashore.

A funny thing happened during the last two hurricanes that hit our town. Every area the insurance folks said would flood did. And the areas that were "X" zones (those they said wouldn't flood) didn't.

There are two things you should take away from this.

One: If you can, avoid any areas that aren't "X" zones. Believe me, that will make your life a whole lot easier.

And two: Never bet against an insurance company's predictions. If it says it will happen, it will.

This brings us to the topic: annuities.”

I have acquired my first annuity about 12 years ago. Frankly, I had no clue about this type of investment. I had some investment experience with mutual funds and even some stocks with a certain degree of success as my accounts grew (mostly because I have been adding cash,  ) and the same degree of misfortune (because I have been losing money more often than making them,

) and the same degree of misfortune (because I have been losing money more often than making them,  ).

).

I don’t recall who has recommended that investment “adviser” but one day the man in his 60-ties came to my house with a lot of promises about the annuities.

I don’t remember Frank’s sale speech (somehow, I still remember his name) but it has resulted in quite a serious investment in annuities – mostly my 401K rollover funds that were not invested into the stocks and mutual funds, yet. At that time, I did not even touch the real estate investments, so, I have decided to invest my funds “wisely”.

Note: Annuities funded with 401(k) rollover or IRA rollovers are qualified plans (tax-deductible) that allow an insurance company to create an IRA annuity where you deposit your retirement funds directly.

I bet that I made this man happy for several days, at least, as he anticipated juicy sale commissions.

Now, thinking about my stupidity 12 years ago, I blame myself for being so naïve. But you live and you learn. Unfortunately, I learned from my own mistakes.

The CORE of Annuities

The core of annuities (as an offered investment choice to the buyer) is a presumption that the buyer will die before the investment company will pay off all the money he has invested upfront. You, as a buyer of annuities, presume the opposite: the insurance company is wrong about when you will go to the “better world”.

The core of annuities (as an offered investment choice to the buyer) is a presumption that the buyer will die before the investment company will pay off all the money he has invested upfront. You, as a buyer of annuities, presume the opposite: the insurance company is wrong about when you will go to the “better world”.

The insurance companies’ business is all about their calculations and statistics regarding the average life span. They assume you will die earlier, so they may keep the rest of the invested money and can stop paying your monthly income. Otherwise, how they can stay profitable?

As S. McDonald indicated, “You can bet the insurance companies have figured out how to work that option to their advantage as well. And unlike with flood zones, making repairs after the fact is not an option with annuities.

The bottom line is that insurance companies rarely lose. You have as much of a chance of beating them at the annuity game as folks who live in flood zones without flood insurance have a chance of "beating" the flood...

They'd better own a boat.”

When you buy an annuity, you are insuring your future income along with your capital. As you know, most insurance products are expensive, and annuity is not an exclusion.

In general, annuities are considered dreadful products, however, depending on your situation, they may fit well into your retirement portfolio.

If you consider annuities but still doubt whether you will make the right decision, consider also a new rule that passed by the Department of Labor in 2016. The rule makes the salespeople and investment advisers fiduciaries. A fiduciary has a legal responsibility to do what’s best for their client and not for themselves or their companies.

If you buy the annuity, make sure you are working with a fiduciary. Unfortunately, most insurance and stockbrokers are not fiduciaries. If they will sell you any financial product that is “suitable for your situation” but costs a lot in the long run, it is your own fault.

I have learned that after passing the rule, the sales of annuities fell more than 15%. Guess why? Because many investment brokers want to avoid the trouble if the customer will complain, not to mention the increased amount of documentation to prepare.

At first, the investment broker “sings a sweet song” about guaranteed income during your retirement years. Isn’t it what all of us want?

You bet I want it now, as I have just said goodbye to daily traffics, office politics, and lazy bosses adding about 9 hours a day to my personal life.

When you think about that sweet promise of income from annuities, you assume that this is a good idea and you will be doing a favor to yourself in the future. The problem is that when it is too good to be true it usually is!

You must know about the real cost of it in the long run, up until the annuity payments will start arriving at your mailbox. Even more, learn about the recurring cost during your retirement years and after your passage to a “better world”.

Let’s Get Educated About Annuities

After reading the previous two chapters, you may ask why should you even learn more about annuities if it's the worst kind of investment?

After reading the previous two chapters, you may ask why should you even learn more about annuities if it's the worst kind of investment?

Don’t hurry up, the annuities still can find a place in your retirement portfolio if you know how to use them properly.

As I have mentioned in my previous articles (see the Investments category), I have made a lot of mistakes as a novice investor. Some of them are associated with annuities bought a long time ago without a thorough understanding of the conditions. However, at this point, as I have retired, I am glad I have several of them that will add a good chunk to my family income.

Annuities are a complicated investment vehicle that can be described by many different formulas depending on the type of annuity. If you “google” the words “annuities equation” under Google images, you might be frightened as there are so many of them, and they seemed quite complicated. It would look like this:

Don’t worry, I am not going to check your math skills but rather try to use plain English.

There are 5 types of annuities, and which one is better for you depends on several variables, including your risk orientation, income goals, and when you want to begin receiving annuity income:

| ANNUITY TYPE | PRO | CON | FEES |

| Fixed Annuity | Straight forward | Pay-less | None |

| Variable Annuity | Offers maximum stock market exposure | May lose principal | Highest |

| Fixed Indexed Annuity | Market Exposure with no risk | Participation rates, etc., diminish the potential for gain | Mid-level |

| Immediate Annuity | Pay highest | Must sacrifice principal | None |

| Deferred Annuity | Cheaper and enable timing of payments | Must sacrifice about how long you will wait for income | Mid-level |

Any annuity is an insurance contract that offers guaranteed income, often for life, and sometimes with small capital appreciation. An annuity is designed to supplement your income (like Social Security, stocks/bonds/mutual funds, etc.).

You may allocate some part of your portfolio to it but don’t invest a lot since an annuity is essentially illiquid (the same as a long-term CD).

There are many considerations before buying the annuities. But the first rule of thumb is “Learn the slang and the meanings”.

Learn the conditions: withdrawals, early withdrawals, terms, early fees, how the interest is compounded if any, what are the guarantees for life or after passing away, and the most important measure -- the fees that can eat away a big chunk of principal.

If you are thinking about the death benefits attached to a contract, make sure you understand that it will come with increased yearly fees.

Most of us hate reading the tiny font in the Terms and Conditions. It is the case when you have to change your attitude and approach. If you are confused with all those crazy definitions, ask for professional advice but not from the salesperson who tries to sell annuities.

Key definitions:

Don't be scared by the definitions. Rather, be patient, and you will get it, I promise.

| Annuitant | The person, usually the contract owner, to whom an annuity is payable and whose life expectancy is used to calculate the income payment. |

| Annuitization | The conversion of the annuity principal to a higher, often lifetime income stream. |

| Beneficiary | A person or persons who receive payments in the event of the death of the annuitant. |

| Contract Fee | An annual fee, among others, is paid to the insurance company for administering the annuity. |

| Contract Value | The cash value of the annuity. |

| Death Benefit | The payment to the annuitant’s beneficiaries in the event of his or her death. |

| Free-Look Period | A specified number of days (e.g., 10 days) during which an annuity contract owner may revoke the purchase of an annuity without penalty. |

| Living Benefits | The guaranteed lifetime income is paid on lifetime income annuities. |

| Period Certain | A feature on some annuities that pays income only for a specific time (e.g., 10 years). |

| Roll up rate | A bonus rate is paid to buyers of many variables and fixed indexed annuities who refrain from withdrawing income for some time, usually at least one year. These rates tend to be very high. |

| Split Annuities | A combined purchase of two annuities, usually involving an immediate annuity, to boost an annuity income stream. |

| Subaccount | The name for mutual funds is offered in variable annuity contracts. |

| Surrender Charge | The cost to a contract owner for sizable or complete withdrawals from the annuity contract before the end of the surrender charge period — typically 7 to 16 years. The earlier the withdrawal, the higher the fee. Many annuities allow the annual withdrawal of 10 percent of the principal, sometimes more, without penalty. |

FIXED ANNUITIES: no-cost, modest, and guaranteed fixed interest investment offered by insurance companies. The interest is higher than CDs from the banks with an option to defer income for several years or draw right away.

VARIABLE ANNUITIES: usually, the basket of mutual funds with an option to capture not only guaranteed income regardless of market performance but also get some capital appreciation if the market performs well. The danger of losing the principal if the market performed poorly is a major drawback. However, in recent years, investors have poured as much as $141 billion into variable annuities.

FIXED-INDEXED ANNUITIES: the annuities with a variable rate of guaranteed minimum interest benefits that are added to the contract value in the case when the market-based index (Russel 2000, S&P 500, etc.) is positive. A drawback: upside potential is “capped” with by a so-called “participation rate” when your return in a rising stock market is trimmed (no matter how well the market performed). Juicy for insurance companies, right? This type of annuities is safer than variable annuities and allows capture of some level of potential market appreciation with downside protection of principal.

IMMEDIATE ANNUITIES: the buyer gives the insurance company some amount of cash that never will be repaid back in return for regular income payments until death. Income payments can be typically higher than other annuities because they are based on principal +interest, and also offer advantageous tax treatment. No fees are attached.

DEFERRED ANNUITIES: they delay payments until a certain date. In my case, as I have described above, I bought them in 2015 and will be able to get the first payments in 2019. Because the insurance company has several years to use your money for free and still charge the fee (!), the payments can be slightly increased (i.e. 5% step-up). These types of annuities may appeal to buyers who want guaranteed income in the future. Everyone’s situation is different. For instance, you have sufficient funds to support your life for several years, and you want the safety of annuities with a guaranteed income after several years when you need it.

Let’s consider three major PROS of annuities:

- They are tax-deferral

- They guarantee the safety of principal (for some types of annuities) that will be paid off to your heirs after your death (if you choose that option).

- They guarantee a minimum rate and even some step-ups if you hold the investment long enough regardless of interest rate fluctuations.

Other PROs:

- With certain annuities, you will never outlive your money

- An annuity may help you better sleep at night during your retirement years.

- Annuities can be integral into estate planning (i.e. death benefit guarantees, the appointment of the beneficiary to avoid probate, etc.)

Now, let’s review the CONS of this type of investment:

1) Long-term performance is ridiculously low (if any at all!). The investment companies use your money to invest in ridiculous proprietary investment vehicles that cannot be even compared to S&P 500 performance. It is like comparing the speed of the turtles with the wild horses.

2) As I said above, it is a completely illiquid investment with a hefty penalty fee for early withdrawal. You also cannot withdraw a lump sum from your annuity.

3) Yearly fees eat your money alive.

Example from AXA annuities:

- Total Investment Performance: $1,747.79

- Less: Contract Fee ($30.00)

- Less Guar withdrawal benefit for Life charge ($151.12)

- Less: Modified Death Benefit Chg ($74.25)

Net Investment Performance: $1,492.42

The result: the AXA has stripped 15% from your annuity’s performance!

4) Getting more benefits (like death benefits) will cost you dearly for the duration of the annuity (see the second example below).

5) As you can see in the table above, you can lose the principal!

6) Time restriction on when you can start withdrawals.

7) Annuities limit how much upside you can make in a bull market not to mention that the purchasing power is being reduced with inflation unless indexed annuity is selected.

8) Possible loss of investment value due to an early death.

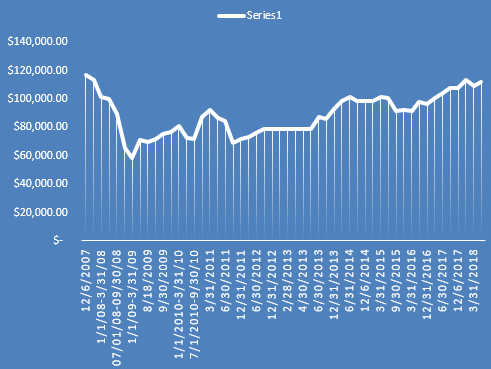

I have purchased another annuity in 2015 in anticipation of my retirement in a few years. The investment company will permit me to withdraw money no earlier than after 5 years since my investment date.

Please pay attention to the time restriction notice. It plays important role in your retirement strategy.

Buying earlier than 4-5 years before retirement makes no sense. Just imagine if I have invested my $150K in the S&P 500 Index fund I could generate a nice return!

At the beginning of 2007, SPY had a value of around $140 per share, and today it is $291.7 (middle of September 2018). It’s a 208.3% difference.

At the same time, look how my $112K Accumulator Plus account from AXA Investment has performed during the same years:

I have about $111.6K after about 10+ years of investment!

Would you be happy with it? I have missed the chance to get the return of $233,296 for the same period if I would rather invest in SPY (S&P 500).

If I would be more knowledgeable at that time, I could rather invest in preferred stocks, some CEFs, BDCs, and REITs that provide nice income. With DRIP, I could be even in better shape. Even index investing could generate a much nicer return.

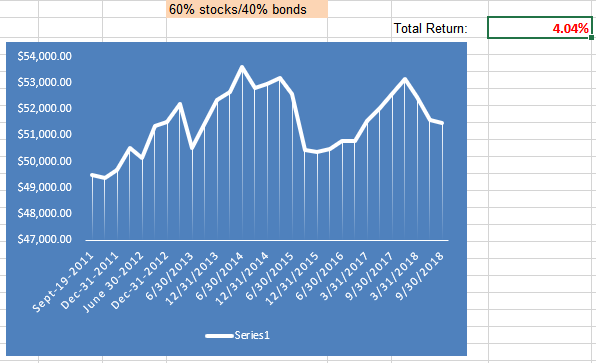

Here is another example of an annuity from Delaware Life: Master Flex II Variable Annuity (see the picture below). Eight years of investment with a 60/40 rule gained a shameful 4.04% return on investment. This investment guarantees a lifetime of 4% income including death benefits from the ending account value based on the market deviations. There were quarterly fees averaging $220/quarter. Since acquiring this annuity, the company has charged $220 x 4 quarters x 8 years=$7,400, not to mention that the company has invested that money in the open market, and was making thousands more.

Here is another example (click on image to zoom):

Do you still feel warm to annuities?

When do you want to buy the annuities?

Annuities still make the most sense for pre-retirees and retirees who want to minimize worry about bear markets in retirement: a precise stream of income no matter how markets perform. Annuities, in short, represent certainty in an uncertain world. Continue to Part II of this article.

If you like what you read and want to be notified about future articles, please subscribe for FREE (at the bottom of a page)